Logistics & warehousing - a new menu fall, but also speculative constructions

During the past weekend summit in London financial leaders of the G20 identified too much acceptance of risk and inadequate remuneration of officials of banks benefiting from the state aid as the main cause of the financial crisis. There was even calling for reform of the banking system and harder sanctions against the so-called tax heavens. Is it possible to challenge this argument or is the sector called „state within a state“ living, among others, from the accumulation of money, the real culprit?

Instability of development is also strengthening by unreadable trends. Perhaps never in the past 60 years statistics or forecasting was such risk disciplines like now. Their protagonists operating in the economic, banking and the real estate sector avoid the definition of longer-term trends for their volatility and also increasingly still more often divergence. The prevailing pessimism in constantly alternating expectations is evident and from a closer perspective the development seems to be unstable.

Credit capacity of banks is limited

Caution of financial institutions remains – their

ability to credit the corporate sector is limited, because of the deterioration

of its financial condition, and an upturn will not come so soon. At least

according to the National Bank of Slovakia, which recently claimed that the

Slovak economy has had to reach the bottom and has the worst behind. In

connection with the decrease in investment activities warns that the demand for

longer-term loans, risk of which also shows the growing number of the so-called

bad loans, clearly declined.

Caution of financial institutions remains – their

ability to credit the corporate sector is limited, because of the deterioration

of its financial condition, and an upturn will not come so soon. At least

according to the National Bank of Slovakia, which recently claimed that the

Slovak economy has had to reach the bottom and has the worst behind. In

connection with the decrease in investment activities warns that the demand for

longer-term loans, risk of which also shows the growing number of the so-called

bad loans, clearly declined.

Since the beginning of the reduced ability of banks to offer loans there was a shift of prime yield (income of properties of the highest category) on the totally 146 basis points – the most scored industrial sectors (180), office (168) and finally retail real estate (106). However, in the 2nd quarter was their total increase by only 7 basis points, of which the industry experienced the increase of 15, offices by 7 and retail only by 4 basis points. All of them – paradoxically – enjoyed a high stability. Most, however, the retail sector, what reflects the greater confidence in its less risky profile and causes less and less willingness of owners to sell it.

The mood in the Slovak industry got slightly worse in August once again. The confidence indicator moved from July's 8.7 points to 9 points after two months of improving (by 18 points). According to the Statistical Office of SR this development was affected by the decline in industrial production, which is expected next three months. Activity in the industrial real estate sector is on the freezing point, but the pessimism can now disperse, by Cushman & Wakefield officials, the expected economic recovery as well as pressure to companies to provide the most modern logistics platform. Growing is expected just in the logistics sector despite the continued dominance of office properties because of investment risk level of this activity.

Either the sphere of logistics and storage facilities, however, does not enjoy anti-crisis immunity. Continued turmoil in global financial markets, according to the recent report of CB Richard Ellis (CBRE), did not go either around it. In Slovakia, in particular, reflected in the low supply of new spaces and a continuous decline in speculative based projects.

Less completed spaces and spaces under construction

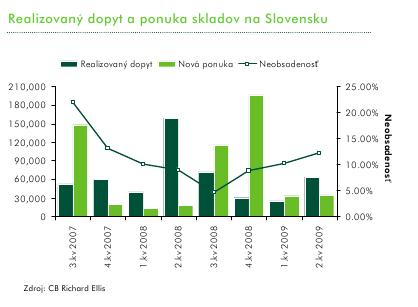

In the second quarter of 2009 was the real estate

market with logistics provided by 35 050 m2 of new warehouse spaces, which

represents the semi-year increase by the modest 2.5%. After the high volume of

new logistics facilities, which enriched the market in 2008, remained a new

offer during the 1st half of 2009 to a low level (13.5% of the total new volume

in 2008). Such a sharp decline should be attributed not only to the influence of

global economic recession but also the amount of spaces completed by the end of

last year.

In the second quarter of 2009 was the real estate

market with logistics provided by 35 050 m2 of new warehouse spaces, which

represents the semi-year increase by the modest 2.5%. After the high volume of

new logistics facilities, which enriched the market in 2008, remained a new

offer during the 1st half of 2009 to a low level (13.5% of the total new volume

in 2008). Such a sharp decline should be attributed not only to the influence of

global economic recession but also the amount of spaces completed by the end of

last year.

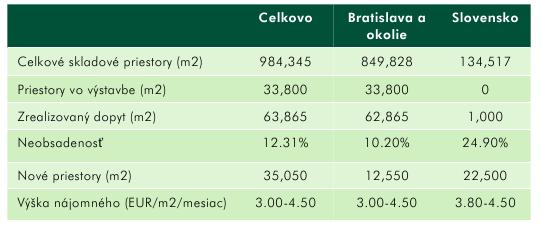

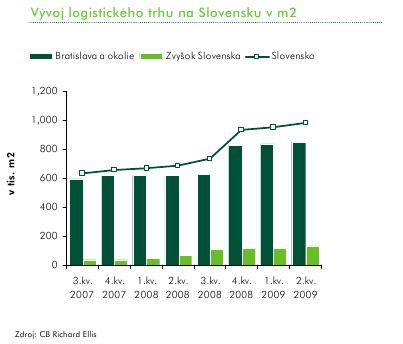

From the total amount of storage space in Slovakia 984.345 m2 at the end of the 1st quarter of 2009, 84 % – portion takes Bratislava and the surrounding area (849 828 m2), located mostly along D1 and D2 motorways. Outside the wider surrounding of the capital they are 134 517 m2 of them. The slowdown in the implementation of new transactions has led to increased non-occupancy rate up to 12.31% (semi-year increase by 2.1%).

Regarding the offer, projects under construction represented only 12% of the number of projects under construction in the same period of last year. The decrease in the volume of spaces under construction continued in the 2nd quarter of 2009 to 38 000 m2, what is the semi-year decrease by 58%. Noteworthy is the fact that 100 percent of the total areas under construction create, according to CBRE, speculative logistics premises in Bratislava and surrounding.

Under construction is 33 800 m2 of storage space, what represents the semi-quarter decrease by 69% and the significant semi-year decrease by 89%. Under construction is the Logistics centre Bratislava – Ivánka of Profin Company (2 800 m2) and PointPark Bratislava of Pinnacle Company (31 000 m2) situated next to the D2 motorway northwest from Bratislava (exit to Lozorno). In both cases, according to CBRE, speculative projects are concerned. It is also worthy the already built-up speculative warehouse spaces with the area of 22 500 m2, which completed Immoeast at Nové Mesto nad Váhom.

The increase in realized demand: 8 of 9 transactions in Bratislava and surroundings

The second quarter of 2009 brought the semi-quarter

increase of realized demand by 40% and the totally 8 transactions conducted in

the total volume of 63 865 m2, by which reached the average of the quarter

demand in last two years. Relative the most contributed the Pinnacle Company

with 28 000 m2 leased in the area of PointPark, what increased the average size

of one transaction on the Slovak market to 7 983 m2. Greatest – 44-percent

market share – achieved just this firm, the second in order was ProLogis with

33.25% of the total volume of transactions signed.

The second quarter of 2009 brought the semi-quarter

increase of realized demand by 40% and the totally 8 transactions conducted in

the total volume of 63 865 m2, by which reached the average of the quarter

demand in last two years. Relative the most contributed the Pinnacle Company

with 28 000 m2 leased in the area of PointPark, what increased the average size

of one transaction on the Slovak market to 7 983 m2. Greatest – 44-percent

market share – achieved just this firm, the second in order was ProLogis with

33.25% of the total volume of transactions signed.

It can be noted that 8 of 9 transactions were realized in Bratislava or in the wider surrounding. The only rental transaction recorded outside Bratislava occurred in the range of 1 000 m2. The rate of non-occupancy was 10.2%, at the end of the reporting period, what is the annual increase by 1.8%. In other words – it is available to approximately 86 700 m2 of outdoor areas. The amount of net leases within the industry remained in Slovakia, according to the findings of CBRE, is currently stable and, momentarily after a slight drop in the best areas in Bratislava and the wider area, ranges from 3.40 to 4.50 € / m2 / month – depending on location, length of lease and free competition.

In spite there are several planned projects, none of them is currently under construction. Looking forward it is expected that the banking restrictions in financing the construction of warehouses and logistics facilities will continue and support the pre-negotiated, but will brake the longer leases, as well as new constructions. If the demand for storage spaces will not increase and the rate of non-occupancy will not drop, a significant proportion of land designated for the construction of logistics will remain unmanaged.

Graphs and a table – CB Richard Ellis

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook