“A-class“ offices hit by weakening demand

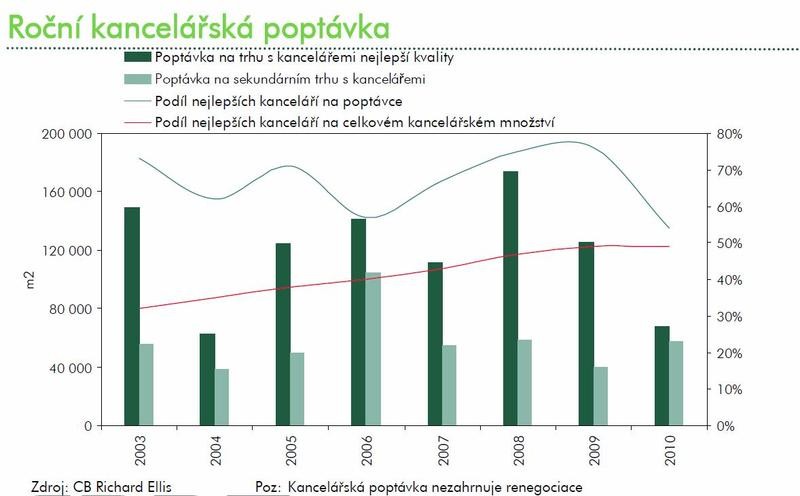

The quantity, or the space, of superior quality offices in Prague has significantly grown during the past decade. At the same time, the figures showed that the proportion of A-class offices on total demand is usually by 20 – 30 % higher than their share corresponding to total supply of administrative buildings in Prague. The crisis has changed this situation dramatically, however.

At the time of strong economic growth there is logically demand for the best market can offer – and A-class offices usually offer unique location and accessibility, large floor space, flexibility and space efficiency allowing for possible future expansion as well as superior technical standards such as air-conditioning, raised floors etc. All this attracts tenants who are less sensitive to the price of rent at times of prosperity. This was true here until 2008.

Crisis decreases interest in quality

Nevertheless, the situation has changed during the

economic downturn. Falling demand, in particular, hit mainly superior quality

offices, while the secondary office market has maintained a relatively stable

interest of tenants. The consequences of slowing demand, recorded already in

2009, were even more visible in 2010. A minimum number of new foreign companies

entering the Czech market has been recorded. The companies already settled here

thus expanded only exceptionally and started to prefer renegotiation rather than

relocation and the demand for A-class offices declined. Its share on total

demand in 2010 reached only 55 %, which is roughly equivalent of the proportion

of superior quality offices in the global supply of admin buildings in

Prague.

Nevertheless, the situation has changed during the

economic downturn. Falling demand, in particular, hit mainly superior quality

offices, while the secondary office market has maintained a relatively stable

interest of tenants. The consequences of slowing demand, recorded already in

2009, were even more visible in 2010. A minimum number of new foreign companies

entering the Czech market has been recorded. The companies already settled here

thus expanded only exceptionally and started to prefer renegotiation rather than

relocation and the demand for A-class offices declined. Its share on total

demand in 2010 reached only 55 %, which is roughly equivalent of the proportion

of superior quality offices in the global supply of admin buildings in

Prague.

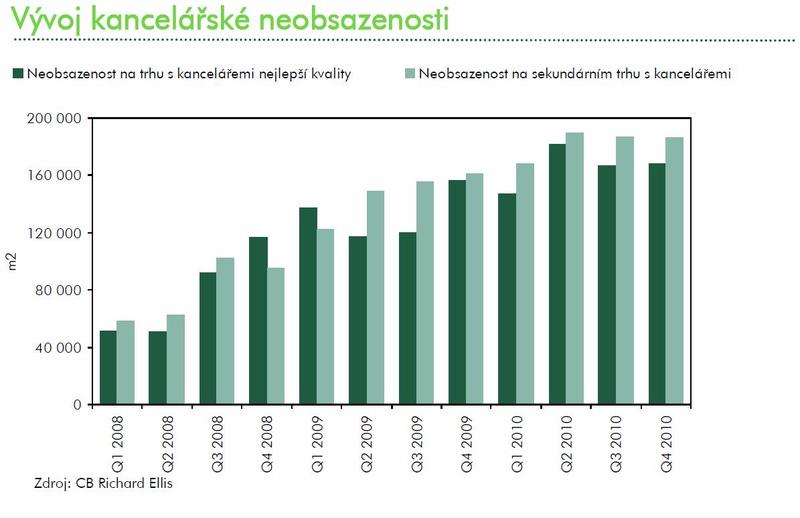

The objection that the weak demand for these offices is caused by their limited supply due to low construction in the past two years (mainly due to strict financing from banks) is not relevant. As shown in the chart, nearly 50 % of vacant office space in Prague (total vacancy rate is 13.4 %) falls into the superior office category. It is clear that since the beginning of the recession and housing crisis, vacancy rate has been gradually increasing in both markets. While the rise in the secondary market was due to tenants leaving the office space, the A-class market vacancy rate growth was caused by growing supply of newly completed buildings. This is also evidenced by the fact that approximately 60 % of vacant A-class offices (nearly 100,000 sqm) are located only in nine buildings. They are mainly speculative large-scale office projects built and completed during the economic downturn.

Market expectations

We believe that renegotiations will remain high in the medium term. Impacts of company cutbacks on the market and the intensity of demand will thus remain visible, the companies will rather use the money saved on leases for their future development. In other words, the companies, which may have been considering relocation three or four years ago due to favourable market conditions, will rather opt for renegotiation today in order to maintain their profitability. This is also fueled by less friendly offers of the best offices landlords, which are no longer so favourable for tenants. In contrast, the extent of incentives on the secondary market grew even more last year including the fact that tenants can negotiate more flexible length of the lease.

On the other hand, we expect business expansion and new companies entering the Czech market due to the gradual economic recovery.

In our opinion, the demand for secondary offices will maintain at a stable level as it will mainly be supported by local companies moving to new premises from C-class offices. Domestic companies are usually more cautious in terms of costs and prefer B-class offices because of the favourable price-to-quality ratio.

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook