Colliers International: Investors discovering “New Europe region“

Colliers International, leading international real estate consultancy company, whose Slovak branch is a member of Bratislava Research Forum (BRF), has focused on 12 markets, referred to as “New Europe region“. Albania, Bulgaria, Croatia, Czech Republic, Greece, Hungary, Poland, Romania, Russia, Serbia, Slovakia and Ukraine were subjected to mapping which resulted in a summary of all commercial real estate sectors in the said countries in 2010 as well as predictions regarding trends projected for 2011.

Stabilization of national economies continues

Let´s start with one important finding:

stabilization of national economies in that region continues, according to

Colliers International (CI). In average forecast, a positive growth of GDP by

3.6 % is also expected by the end of this year. Expansion, as the survey

identified the trend, is based on a combination of high growth in industrial and

processing and falling unemployment.

Let´s start with one important finding:

stabilization of national economies in that region continues, according to

Colliers International (CI). In average forecast, a positive growth of GDP by

3.6 % is also expected by the end of this year. Expansion, as the survey

identified the trend, is based on a combination of high growth in industrial and

processing and falling unemployment.

On the other hand, several concerns need to be taken into consideration. Inability to pay government bonds, austerity measures, growing inflation (approximately 6.1 % in 2010, a similar figure is expected for this year), costs of international debt or prices of energy, food and basic commodities, which may hinder any greater economic expansion and flip upside down the favourable prognoses for this year, although in varying degrees in different countries.

Investment market in CEE reviving

In comparison with 2009, there was a significant recovery last year in terms of volumes of transactions in the investment market in the New Europe region. This is a 47 % yoy increase to EUR 6.36 billion. Even after considering market cycles, there is still something missing in long-term turnover in the financial volume of EUR 10 billion representing only about 7.3 % of total transactions in Europe.

Investors´ interest during the search for acquisition opportunities, which should increase the volume of turnover in the regions, continues to move from the so far dominant V4 and Russian markets towards the south and east of Europe. CI cites an example of sale of a first-rate office building worth EUR 100 million in Bucharest, which was executed at the end of 2010. This was the first major transaction in this market since 2006.

“While the transaction cycle is on the way back up, the future in 2011 is somewhat unclear,“ CI survey states. At the same time, the authors didn´t miss the trend of money shifting from the main markets in Poland and Prague.

Offices: rents for the highest standards to return to their original level

It is getting clear that the vacancy rate in these

countries peaked and it will face a period of stagnation or slight decline

during 2011, the survey states. Although average rent is likely to remain stable

throughout the year, soon we will see an increase in the highest rent achieved

for first-rate premises in the best locations (prime rents).

It is getting clear that the vacancy rate in these

countries peaked and it will face a period of stagnation or slight decline

during 2011, the survey states. Although average rent is likely to remain stable

throughout the year, soon we will see an increase in the highest rent achieved

for first-rate premises in the best locations (prime rents).

Kiev is a simple example. At the end of 2010, the local prices returned to their original level after a 50 % fall. Warsaw can probably expect a similar trend in the first half of this year. It will last at least until the end of the year when the highest rent achieved in first-rate premises in the best locations will return to its original level also in the other markets. It will be due to levelling of excessive supply and a limited addition of new space.

Industry: growth of production and decline in vacancy stimulated demand

A significant growth of industrial production in 2010 stimulated demand for modern storage and logistics space. This shift was visible mainly in Poland, Czech Republic and in the Moscow region, and it was boosted by a decline in vacancy in these regional markets.

Besides these three, however, weak demand for industrial real estate in the New Europe countries continued, according to CI. Certain downside is insufficient vicinity of the market – export partners are in Western Europe, especially in Germany. “At the end of 2010, developers´ interest in land in Slovakia also revived, but this interest is moving further south or east. Many markets will therefore be fuelled by demand for retail space on a short-term basis,“ authors of the survey suggest.

Retail: uncertainty remains, long-term prospects more positive

Uncertainty about the occupancy of the retail sector

continues. Retail sales suffered during the crisis . Austerity measures adopted

by governments keep domestic consumption in Poland and the Czech Republic at

unusually low levels compared to normal values. According to CI, this will last

for another year until retailers reach the level that would encourage further

expansion or increased rents.

Uncertainty about the occupancy of the retail sector

continues. Retail sales suffered during the crisis . Austerity measures adopted

by governments keep domestic consumption in Poland and the Czech Republic at

unusually low levels compared to normal values. According to CI, this will last

for another year until retailers reach the level that would encourage further

expansion or increased rents.

Long-term prospects sound much more positively mainly due to doubling of the growth forecasts for Western Europe until 2020. A large number of international retailers who will enter the New Europe region make the outlook of occupancy positive. However, at the same time they will place a higher demand on the quality of shopping centres with top-quality premises, Colliers International points out at the end. According to The Lipsey Company and National Real Estate Investor magazine, CI is the world´s number two among the best commercial real estate brands, it has more than 15,000 professionals working in 480 offices in 61 countries.

Source – Key Communications

Map – Part of New Europe region, including Ukraine

Photo 1 – Bratislava (Colliers International)

Photo 2 – Bucharest (Wordpress)

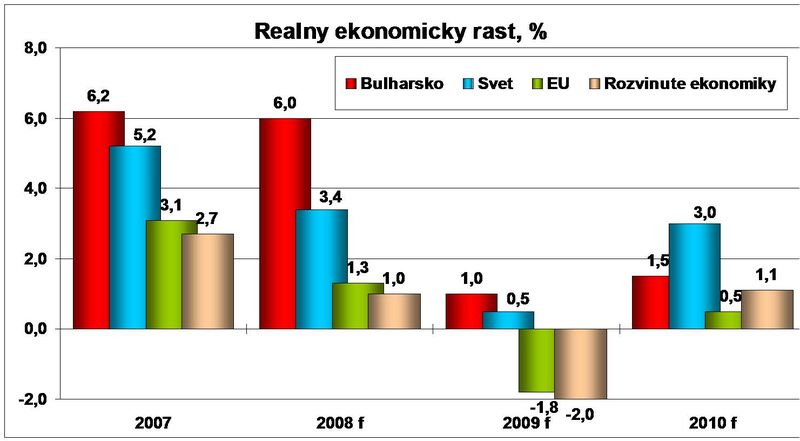

Graph – Course of the global crisis in Bulgaria, EU and the world

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook