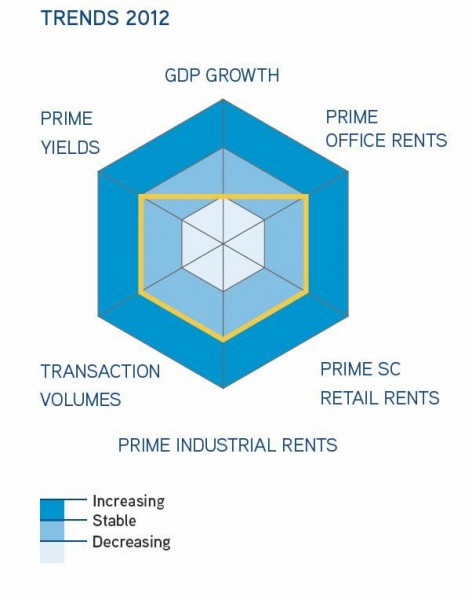

Stability is the name of the game

Stability is the name of the game on the Czech Republic real estate market in 2012. This is according to the recently published annual report by Colliers International, 2012 Eastern Europe Real Estate Review: Czech Republic. The report provides a summary of 2011, an examination of recent trends, and prognosis concerning the office, retail, industrial and investment markets of the Czech Republic in 2012. The report also comments on the economic conditions within the country, as well as its proximity to Germany, in relation to overall future outlook.

“The Czech Republic is a relatively stable economy with a well capitalised and regulated banking system,” says Omar Sattar, MRICS, Managing Director, Colliers International Czech Republic. “As foreign banks with a local presence pull back on lending this year, local banks are in a good position to partly fill this void and we could see the emergence of specialised debt funding vehicles entering our market.” “Czech exports are positioned to benefit from an improving German economy in late 2012 or early 2013,” added Mr Sattar. “As Germany grows, this has a positive effect on the Czech Republic.”

Some highlights of the different market sectors are as follows:

Key Investment Market Data – Czech Republic

| Investment Turnover | €2.2 billion |

| Prime Office Yield | 6.50% |

| Prime Retail Yield | 6.35% |

| Prime Industrial Yield | 8.00% |

On the investment market, 2011 investment transactions totalled more than €2.2 billion closed in the Czech Republic – around four times higher than 2010. The return of foreign investors to the market is believed to have bolstered the already active Czech based investor group; the share of total transactions by Czech investors decreased to 28% in 2011; however the absolute volume of their investments increased to €570 m from €390 m in 2010. Investment trading volumes in the coming year, however, are unlikely to reach the figures posted in 2011. This is mainly to be blamed on debt deleveraging as banks attempt to clean up non-performing loans in their portfolios, as well as ongoing Eurozone uncertainty.

Key Industrial Figures – Czech Republic

| Total Stock | 3,946,500 sq m |

| Take-up | 816,800 sq m |

| Vacancy | 7.7% |

| Prime Headline Rent | € 4.40 sq m/pcm |

Industrial stock expanded by 240,000 sq m to 3.94 million m2 in 2011; a 6% increase compared to 2010. The logistics sector accounted for a 55% share of gross take-up, while 28% of total leasing activity came from the manufacturing sector. However, looking at demand in terms of net take-up, the logistics sector represented 44% and the manufacturing sector accounted for 36%. The geographic clusters of Czech industrial stock saw a change in their ranking based on proportion of total stock, with Southern Moravia overtaking Western Bohemia; Prague holds 1.6 million sq m of Czech industrial stock and is the region with the largest share of industrial buildings. “Speculative development of industrial space was rare in 2011 and when it did occur it often comprised an adjunct to the construction of pre-leased space,” says Omar Sattar. Barring an economic meltdown, vacancy rates are set to continue to fall further, and approximately 160 – 180,000 sq m of new industrial space is expected to come onto the market in 2012.

Key Office Figures – Prague

| Total Stock | 2,800,466 sq m |

| Take-up | 325,564 sq m |

| Vacancy | 12.01% |

| Prime Headline Rent | € 20–21 sq m/pcm |

12 new office buildings were completed during 2011, totalling almost 100,000 sq m; increasing office stock in Prague to 2.8 million sq m. 13 projects, totalling 127,400 sq m of new office development were under construction in 2011, most of which should be completed by the end of 2012. 2011 was a record year for gross office take-up, and prime rents remained unchanged. In 2012, 11 buildings, representing 113,000 sq m of office space, are expected to come on to the market, 65% of which will be located in Prague 4 and Prague 8. 2012 take-up levels are unlikely to reach the demand levels of 2011 and it is expected that share of renegotiated leases will increase as tenants reconsider expansion or relocation. Levels of speculative development are expected to drop in 2012 due to banking restrictions on development financing. Office rental rates are anticipated to remain flat throughout 2012; however, net effective rents could rise from their current levels of 10–15% below quoted headline rents as vacant space around Prague dries up.

Key Retail Figures – Prague

| Total SC Stock | 870,000 sq m |

| Prime Headline SC Rent | € 170 sq m/pcm |

| Prime Headline High Street Rent | € 90 sq m/pcm |

A limited number of new shopping centres came to market in 2011; some existing retail properties were refurbished in smaller towns, and several retailers continued to seek space in the best performing shopping centres around the country. According to Mr Sattar, “Popular, well designed shopping malls with a good tenant mix will benefit from rental growth and attract retailers seeking to lease shop units, while shopping malls that have struggled as of late will do well to maintain their current levels of tenant occupancy.” Some new shopping malls will be added to the retailing stock (e.g. Nová Karolina in Ostrava), however retail development is more challenging than other property sectors. In 2012, average rental rates are expected to be stabilized and many landlords will be hoping to maintain, or grow their rental income and move out weaker tenants for stronger existing or new brands that are considering entry into the Czech market.

Source: Colliers International

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook