Bratislava Offices: No new supply this quarter

„2012 has started with solid take-up, although almost half of it was attributed to renegotiations. Due to no supply, vacancy rate decreased and we expect further fall in the upcoming months until the new space will be delivered before the end of this year“, said Oliver Galata, Head of Office Agency CBRE in Slovakia. Total leasing activity in Q1 2012 reached 24,191 sq m, while almost half of this amount was attributed to renegotiations. Overall office vacancy rate decreased slightly by 100 bps q-o-q to 10.2%.

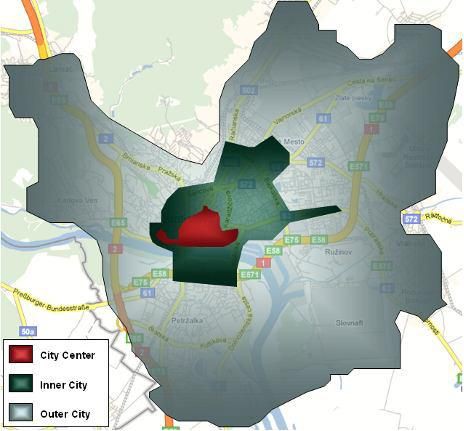

Modern office stock

Bratislava modern office stock currently stands at approximately 1.45 million sq m. The distribution of modern office stock by location at the end of Q1 2012 was:

- City Centre submarket (32.3%), with a vacancy rate of 10.9%

- Inner City submarket (42.3%), with a vacancy rate of 8.6%

- Outer City submarket (25.4%), with a vacancy rate of 12.0%

Newly built schemes (constructed latest in 1998) currently account for ca 70% and refurbishments for 30% of the market. Grade B stock tends to be refurbished office space, which has limited standard of premises (e.g. no raised floors, no air exchange, general appearance of the building etc.).

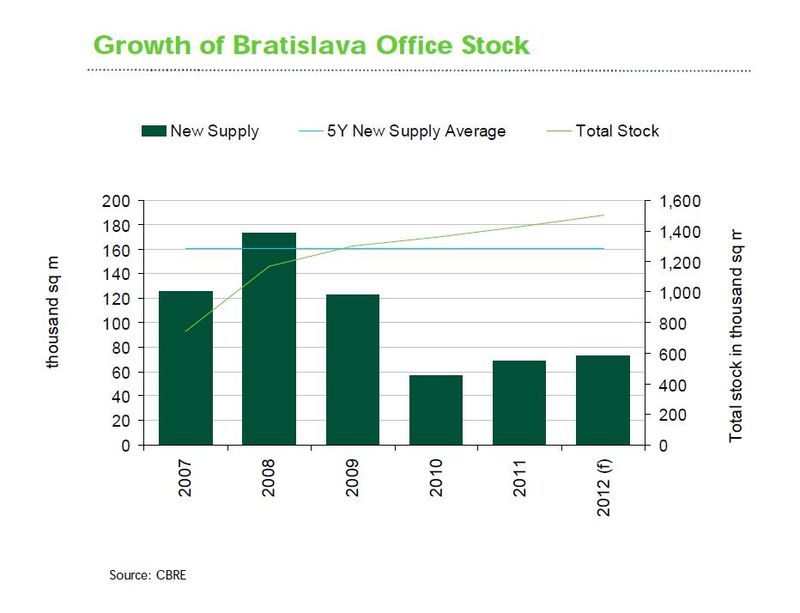

New supply

In Q1 2012 we have not recorded any addition, newly built project or refurbishment, to the existing modern office in Bratislava. However; before the end of this year we will see ca. 72,800 sq m of new office space delivered to the market. All of the projects making up this total are currently under construction.

Total leasing aktivity

Total leasing activity (TLA) on the Bratislava

office market in the first quarter of 2012 reached 24,191 sq m. This is twice

as much compared with the same period last year, however in line with the last

year’s average. Similarly as in previous quarters, a considerable share was

represented by renegotiations (46%), while remaining 54% were attributed to

new deals.

Total leasing activity (TLA) on the Bratislava

office market in the first quarter of 2012 reached 24,191 sq m. This is twice

as much compared with the same period last year, however in line with the last

year’s average. Similarly as in previous quarters, a considerable share was

represented by renegotiations (46%), while remaining 54% were attributed to

new deals.

Following last year’s trend, many tenants are choosing to roll over existing leases or take short-term expansion space as opposed to relocating. We expect this type of transactions to sustain a stable share within the leasing activity on the office market throughout this year.

Only ca. 10% of TLA (2,300 sq m) was formed by occupiers that moved from C-class standard to A/B-class premises, occupiers expanding their premises and new acquisitions coming to the market. This is the lowest amount of net take-up we have recorded throughout the previous year, while the quarterly average has been approximately 8,400 sq m.

Office Market Indicators, Q1 2012

| City Centre | Inner City | Outer City | |

|---|---|---|---|

| Total stock (sq m) | 468,500 | 613,000 | 368,000 |

| Vacant space (sq m) | 51,000 | 53,000 | 44,200 |

| New supply (sq m) | 0 | 0 | 0 |

| Headline rent (€/sq m/month) | 14.00–17.00 | 10.00–14.00 | 8.00–12.00 |

In relation to the distribution of total leasing aktivity in Q1 2012 by location, majority of the area was let in the Inner City Submarket (62%) followed by City Centre (30%) and Outer City Submarket (8%).

In terms of the market share this quarter, the majority of transactions were signed in Professional Services sector (37%), followed by IT sector with 21% share.

Vacancy and net take-up

By the end of this quarter the amount of vacant

space reached ca. 148,000 sq m. This equates to a current vacancy rate of 10.2%

which is higher by 70 bps y-o-y. The decrease is caused by missing new supply

combined with stable demand.

By the end of this quarter the amount of vacant

space reached ca. 148,000 sq m. This equates to a current vacancy rate of 10.2%

which is higher by 70 bps y-o-y. The decrease is caused by missing new supply

combined with stable demand.

This level is slightly lower compared with the average vacancy rate we have measured over the past two years.

Net absorption, which represents the change in occupied stock within a market during the surfy period, reached 17,100 sq m this quarter, representing an increase by 34% y-o-y.

Rents

Achievable prime headline rents for premium office space in Bratislava are estimated at approximately EUR 16.00–17.00/sq m/month in the City Centre location and are remaining stable. In non-prime locations the headline rents are within the range of EUR 12.00–14.00/sq m/month.

Effective rents could be lower by 8%-12% counting with incentives offered by landlords. However, the incentives largely depend on quality, location and vacancy of the individual office scheme.

We do not expect any decline in rental levels in foreseeable future, especially in A-class buildings. However, older generation buildings may see a slight downward pressure on headline rents in the next 6–12 months.

Outlook

For the upcoming two years we expect a continuing low but healthy level of completed new office projects. There is a noticeable recovery on the supply side with few construction starts last year securing a steady supply in 2012 and 2013.

As at the end of Q1 2012 we have monitored 72,800 sq m of office space under construction with completion planned for 2012; mostly in the sekond half of the year. This is in line with the amount of stock brought to market in the years 2010 and 2011.

In terms of the level of demand for office space, we expect this to remain sustainable for the rest of 2012.

Source: CBRE

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook