The world according to CNB: stabilization is the sign of the times

The Czech crème de la crème forecast – the “Financial Stability Report“ by CNB (Czech National Bank) – will probably not give any more wrinkles to the local property development. But it will not remove them either. The entire economy and property market must prepare for more modest times. The basic motto of the latest outlook document by CNB is “stabilization“; in all parametres – at their current, but not always ideal level. The central bank analysts do not rule out an emergence of worse times, they however, consider this “unlikely“.

The overall impression of the “Financial Stability Report“ (FSR) is nonetheless highly optimistic. The prognosis deals primarily with the stability of the financial sector. From governor Tůma´s words (“The Czech financial sector is doing relatively well!“), from the overall tone of the document and the stress tests results it is obvious that the Czech Republic does not need to worry too much in this respect.

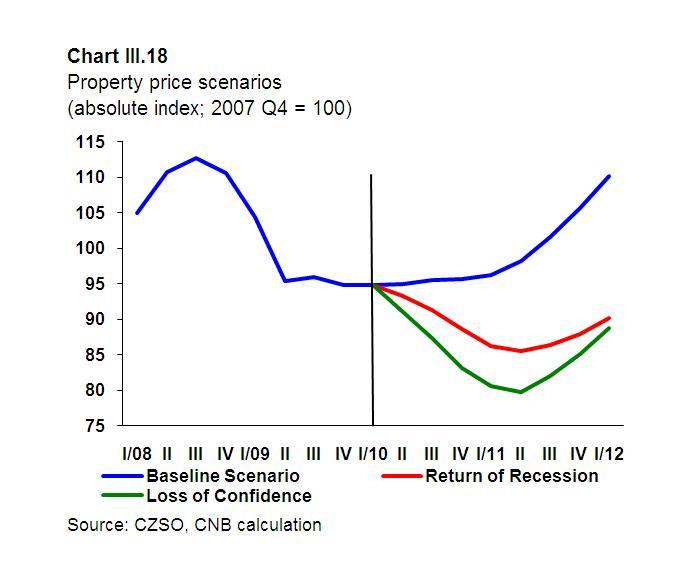

Three development scenarios were created at CNB for the period until 2012: “basic“ which is considered realistic, the second is “return of recession“ and the third, worst named “loss of trust“. The third is based on a combination of weak economic growth (followed by the return of recession) with a crisis in the financial markets and consequently in the financial sector. CNB do not rule out the second and third scenarios, however, their fulfillment is thought to be improbable. According to the FSR, the local financial sector should remain stable and even profitable at any of the development scenarios. Bank profits would, however, fall from the estimated CZK 47 and 63 billion this year and would fall to a little more than CZK 19 bill. in 2011 for both scenarios and further up to CZK 8,3 and 2,6 bill. (scenario “loss of trust“) in 2012.

While the banks and other financial institutions can therefore more or less relax, figuratively speaking, the FSR does not have such a positive outlook for others. On the other hand, the attentive reader can see that, despite the caution and temperance of most formulations, perhaps no real disaster or crisis situation threatens anybody.

Macro background: slow recovery

The macroeconomic environment in which all economic activities of households, companies and the state take place, should be at least bearable in 2010 – 2012, according to the FSR. The central bank calls it “a very gradual recovery“ in their basic scenario. In terms of the development of the basic parameters of the current state of the economy, in short, this means roughly the following: small growth of the GDP (1 – 2 % this and next year), an equally undramatic rise in the unemployment and a bearable increase in prices in the internal market (inflation rate up to 2 % per year) and a stable crown exchange rate (25 – 26 CZK per EURO). If we put aside changes in external environment, then the basic requirements of this relatively decent economic tomorrow include first and foremost ability to manage debt servicing, by everyone, i.e. by the state, companies as well as households.

The state is in the worst situation. Its relatively low indebtness (it amounted to 35 % of GDP at the end of 2009) unfortunately has enormous dynamics. In 2007, the Czech government had “gross borrowing needs“ of CZK 135 bill., it was CZK 280 bill. last year and from 2011 it is necessary to allow for amounts over CZK 300 bill. per year. This is the reason why the FSR emphasises the need for budget consolidation because it is here that CNB sees the highest risk in the Czech economic future. It can be added that the election results and the course of the after-election negotiations are a good start in this regard.

Careful client

The public sector is only an occasional client for property developers (acceleration in the implementation of larger PPP projects cannot be expected). In this case redevelopment of debts (logically connected with lower demand) does not mean a major hazard for them. But what will their private customer, households and companies be like? FSR does not promise developers any significant improvement or worsening in this regard. Assets of Czech households still exceed their liabilities, however, troubles with installment payments exist and will continue to exist. The share of problematic mortgages (unpaid for 90 and more days) is around 5 % today and it is expected to grow slightly over the next two years to 6,5 % (the “loss of trust“ scenario allows for up to 20 %). The number of personal bankruptcies will grow slightly, 8 – 9 thousands of them per year are expected.

It is already clear today that households are less willing to become more indebted due to the state of employment market and overall rising costs of servicing of existing loans. The near future will probably bring overall higher costs for Czech families, possibly through higher taxes, possibly school fees and from the other side, due to reduction of some social security benefits. The resulting current and future slimming of demand will also enhance a rather more cautious attitude of all institutions providing credit.

The same in other contexts will undoubtedly apply to the corporate sphere whose willingness to invest (and for example to lease new or more offices, warehouses etc.) will be also limited by their need to repay debts. The rate of defaulting loans by companies (delay of payments 90 or more days is the basic but not the only and necessary criterion for classification of the debt as such) has increased to the current level of approximately 6 %, however, it should fall again to 2 % in 2012, according to CNB.

In this context, is appropriate to mention the financial or debt condition of the developers themselves. As a whole the local property development sector is a more disciplined debtor than other sectors, however, the opposite goes for residential developers. Already approximately 11 % of their loan portfolio is categorised as defaulted loans. FSR does not contain any predictions in this matter, it only points out forced sales. It expects their increase which should decrease prices furher, but on the other hand, it should set in motion the entire property market.

Residential: another bonanza in two years?

FSR speaks of an approximate fall of 5 % in the residential sector prices for the period since the end of 2007. This was also a reaction to the previous steep soar which culminated in the year 2008 (in relation to the end of 2007, prices increased by 15 %) and which earned the nickname “bubble“. Through close reading and examination of the FSR graphs it seems that it may not have been a bubble – i.e. an enormous and short-term price fluctuation. The basic FSR scenario expects flat and family house prices to return to the year 2008 level some time in 2012. According to CNB, this development is highly probable, the two less favourable models of development which would lead to a further decrease in prices (in relation to today by 8 %, and 16 % respectively) are thought to be “not very likely“.

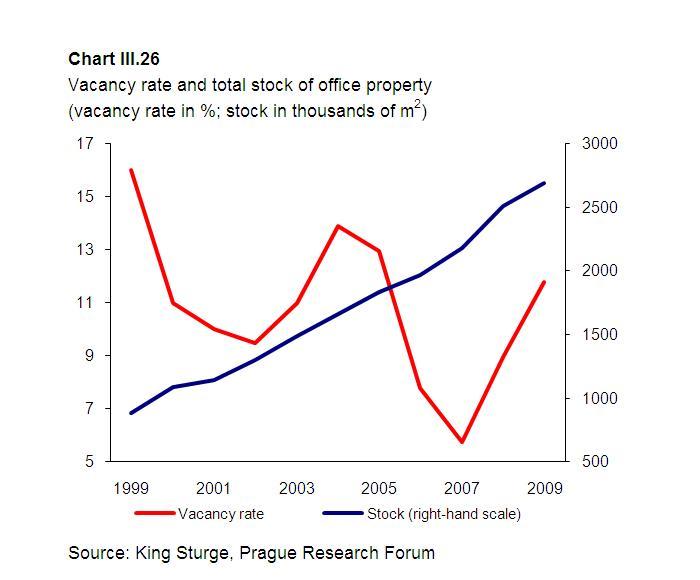

FSR devotes only a short passage to commercial property which charts the current situation briefly compared to one or two years ago. According to the CNB, the commercial real estate market segment is facing a strong slump in demand from investors and users, resulting in decrease in prices and in extent of construction as well as growth in vacancy rate. FSR does not include any outlook for this property market segment, it only expects the already mentioned number of forced sales.

Will it be so?

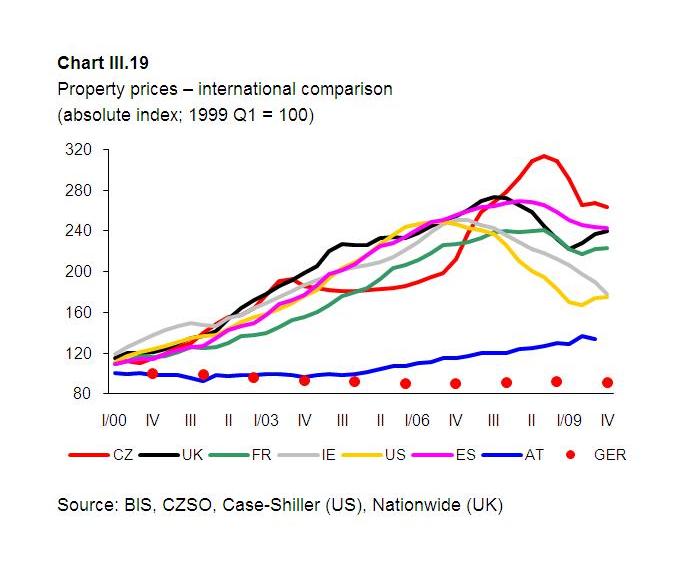

Monitoring and property market research – not to say forecasts for its development – are a problem in our country. A reliable statistical base is lacking, therefore the CNB analysts themselves point out the basic statistical problem of the property market (significant differences in units being compared), in addition to a number of purely “Czech“ problems (short time lines, the differences between listed and actual prices, insufficient monitoring of development in regions etc.). This is true one way or another for all the sources used in FSR – Czech Statistical Office statistics, IRI, King Sturge as well as price index of professor Dolanský´s from Czech Technical University.

If we applied the above question to the entire FSR report, the tendency towards a positive answer will undoubtedly be stronger. The proviso to say “no“, however, remains possible; moreover the authors of FSR repeatedly warn about this. CNB prognoses are nevertheless the best available in the area of economic forecasting in the Czech Republic. Only there is hardly any economic expert who has not pointed out lately that all prognostic and econometric models are currently failing. And it also often points to the hitherto underestimated factor of economic affairs: mental attunement of its players. Moods, expectations and wishes may among other things also be of a „self-fulfilling“ nature. CNB perhaps along with FSR should also hand out doses of optimism, with “no extra charge” prescription. Maybe what we believe will happen.