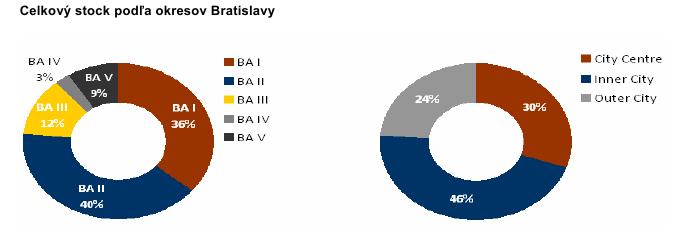

The "office favourite" in the first quarter is Bratislava 2

At a time when some of the analysis tentatively suggests that the curve of the economic crisis could go slowly into decline from the current amplitude, unreachableness of real estate market is growing. This state is indirectly identified by the numerous and increasingly frequent data and numbers in the surveys of consulting companies prudently restricting for their presentation only, while the estimated long-term trends rather avoid. Similarly is designed the latest report of Bratislava Research Forum (BRF) on the results of the office spaces market for the first quarter of 2009. The association of three companies operating in the field of real estate consultancy (CB Richard Ellis, Colliers International and Cushman & Wakefield) provides customers and media naked information product and concrete conclusions from it they have to drawn themselves.

On the other hand, all that is not the mission of BRF. Members of the Forum, as they often point out, mutually "share information, which are not confidential in order to provide our clients and public consistent, accurate and transparent data on the market of office spaces in Bratislava. This from purely methodological reasons divides into three parts – the centre, the internal and the peripheral part of the city. Obtained data are also shown as allocated to five Bratislava districts.

Each district excels in something else

Let us finally look at the resulting numbers coming

from the end of the first quarter of 2009. The Office Stock in the capital of

Slovakia exceeded 1.191 million m2 that time, whereas 60 percent of this offer

constitutes standard A and a 40 percent standard B. It is worthy to compare

the status from the end of the 3rd quarter of 2008, when this figure represented

the number of 1.16 million m2 (which is an increase by approximately

31 thousand m2), while the proportion of office „A“ against the „B“

remained unchanged.

Let us finally look at the resulting numbers coming

from the end of the first quarter of 2009. The Office Stock in the capital of

Slovakia exceeded 1.191 million m2 that time, whereas 60 percent of this offer

constitutes standard A and a 40 percent standard B. It is worthy to compare

the status from the end of the 3rd quarter of 2008, when this figure represented

the number of 1.16 million m2 (which is an increase by approximately

31 thousand m2), while the proportion of office „A“ against the „B“

remained unchanged.

26 823 m2 of Office Supply was added in the period from January 01 to March 31. The majority of these – up to 57 percentages – has been approved, as traditionally, in Bratislava 2, followed by Bratislava districts 3 (19%) and 5 (24%), which for example last year excelled in the volume of closed transactions. The primacy of the 2nd Bratislava district is not in the completed Office Supply only, but also that there is placed approving the largest office building – the of Strabag Company building. The centre of Bratislava paradoxically avoided building as the only place: the Office Supply did not enrich here by the only project of a new building.

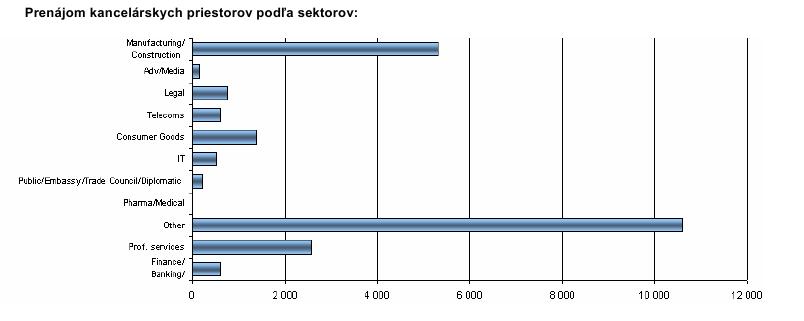

The rental sector "others“dominated

The Office Take-up closed during the first quarter

was not so much successful. Their total volume reaching the area of 23 000 m2

fell by 16 800 m2 compared to the previous quarter. Prevailing were

transactions of companies from the sector „others“ (which can not be

incorporated into the defined typology); other places in the ladder of success

took the sector of production and construction services and the professional

services sector.

The Office Take-up closed during the first quarter

was not so much successful. Their total volume reaching the area of 23 000 m2

fell by 16 800 m2 compared to the previous quarter. Prevailing were

transactions of companies from the sector „others“ (which can not be

incorporated into the defined typology); other places in the ladder of success

took the sector of production and construction services and the professional

services sector.

Majority of the Office Take-up closed the companies with the size of 1 001 to 10 000 m2 – together they rented 12 334 m2 office space (53%). Companies with the size 501 – 1 000 m2 rented 6 280 m2 (27%) and on the third place are firms with less than 500 m2, which rented totally 4 535 m2 (20%) of the office space. The most significant transactions of the first three months of 2009 included Ido Hutný projekt – Lakeside Park I (2 900 m2) and Vodohospodárske stavby – AC Petržalka (1 200 m2).

Lower increase – higher occupancy

The BRF report shows further interesting findings:

decrease of the Office Vacancy to 8.7 percent, which the forum attaches to

relatively greater rate of closed transactions (although semi-quarterly

falling!) than the Office Supply to the market (SPP buildings and Strabag

occupied the companies that have them built-up). It is again the fact, which

cannot be taken as a significant one or to derive from it any generalized

conclusion. Lowest Office Vacancy showed the Bratislava districts 1 and

4 this once.

The BRF report shows further interesting findings:

decrease of the Office Vacancy to 8.7 percent, which the forum attaches to

relatively greater rate of closed transactions (although semi-quarterly

falling!) than the Office Supply to the market (SPP buildings and Strabag

occupied the companies that have them built-up). It is again the fact, which

cannot be taken as a significant one or to derive from it any generalized

conclusion. Lowest Office Vacancy showed the Bratislava districts 1 and

4 this once.

As thus seen, although the speech of numbers seems explicitly and comprehensively, the interpretation of relations and connections between them already requires analytical, distinctive and evaluative erudition. The future of the office segment cannot be wrest from the broader context – real estate, financial, economic or geographic one. Many of last year's prognosis and expectations (such as an increase in rental prices due to high GDP growth and employment or no exceeded demand above offer) no longer apply. They can serve at most like learning points that even the greatest expert is not immune to mistake, what always applies universally and twice just now.

Definitions according to BRF

Office Stock: The offer of buildings approved after 1993 – reconstructed or newly built, in standard A or B, in the lease of the owner or other tenants. Buildings owned by the state and less than 800 m2 are not a part of the Office Stock.

New supply: Reconstructed and newly built buildings in a certain period of time.

Buildings in standard A: The classification includes meeting the above-standard criteria, including an integrated air-conditioning system, limited depth of spaces, minimum clearance of 2.75 m, flexibility of a space, trenches for telephone, data cables, double floors, reception, indoor car access, lifts, access for disabled and backup energy sources.

Buildings in standard B: It includes a typical real estate in the market on the basis of the above-mentioned criteria.

Office Take-up: The gross numbers of the total floor area, which has been leased or sold to the lessee within a certain period of time. It does not contain free space, which remains in the offer. Property is considered as rented on the day of signing a lease or contract for the future lease agreement. While the Total take-up also includes the renewal of leases, net take-up not.

Pre-lease: Active pre-leasing for the office building indicating the phase during which the prospective lessee is offered with specific layout of spaces, whereas the building must be under construction.

Office Vacancy Rate: Percentage expression of free rentable office spaces in the ratio to total offer.

Pre-lease: Active pre-leasing for the office building indicating the phase during which the prospective lessee offered specific distribution areas, the building must be under construction.

Prime rent: The highest rent achieved in respect of new office units with the highest standards and in the best locations.

Illustration visualisation – J&T / Vara Group

Graphs –Bratislava Research Forum © source

Graph n°1 – Office stock allocated to Bratislava districts

Graph n°2 – Lease of office spaces allocated to sectors

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook