Year 2009 will be critical for hotels of the Central and the Eastern Europe

The crisis is preliminary not about to go away and after seldom breaths of tentative optimism it is clear that this was only a part of „tactics“ not to allow an understanding of the rules governing it. After office, residential and logistics segments it neither circumvent the hotel segment, which linkage to real estate and tourist resorts makes its quite specific position even more complicated. The Central and the Eastern Europe is perhaps the only region of the old world that developers despite the continuing pressure of world economic recession did not condemn entirely and continue to see the opportunity to kick-in their investment goals there. Although after years of resolute expansion also here occurred a sharp slowdown in economic growth, the long-term set prognosis mostly predict it a significantly higher GDP growth than in the western part of the continent.

Despite the decline the interest persists

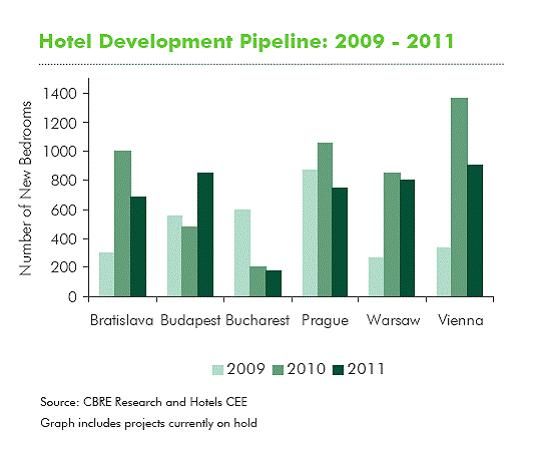

By the latest report of CB Richard Ellis (CBRE), the

launched production remains still high in the countries of the Central and the

Eastern Europe (CEE). The leadership in a number of newly created housing units

in 2009 acquired the Czech metropolis. According to CBRE tightened conditions

in lending capital from banks, however, may eventually cause that the attention

of developers in Prague will be limited only to the ongoing projects, while the

planned would postpone until the credit situation is clarified. The interest of

international hotel brands in the CEE region remains, but advisers pointed to a

certain shift: they are caution and picky in the choice of location and type of

the contract.

By the latest report of CB Richard Ellis (CBRE), the

launched production remains still high in the countries of the Central and the

Eastern Europe (CEE). The leadership in a number of newly created housing units

in 2009 acquired the Czech metropolis. According to CBRE tightened conditions

in lending capital from banks, however, may eventually cause that the attention

of developers in Prague will be limited only to the ongoing projects, while the

planned would postpone until the credit situation is clarified. The interest of

international hotel brands in the CEE region remains, but advisers pointed to a

certain shift: they are caution and picky in the choice of location and type of

the contract.

The Podunajská metropolis Bratislava is to be considered the city with „generous hotel market“, where the average daily rate (ADR) increased by modest 0.3 percent in the last year. The big fall of occupancy in its second half, however, caused reduction in RevPAR (Revenue per available room) – revenues of a sold room by 7.6 percent.

Martin Thomas – Associate Director CEE Hotels reminds: "The tendency in reduction of hotel occupancy level maintained even in the first three months of 2009 and resulted in the decrease of the average occupancy by full 40.1 percent. The decrease in ADR by 5.2 percent, together with the decrease in occupancy reached as per the concerned date and day to an average revenue per available room 37.50 €, which means a full-year drop by 29.6 percent.

Some of planned hotel projects in Bratislava hit the impact of the intimating economy fatally: they fight with the difficulties in obtaining finances, which caused their postponement or even cancellation. By contrast, in the case of the Kempinski Riverpark or Sheraton Bratislava they are successful projects, which will reach their opening in the first half of 2010 as a part of broader regional and functional changes in the central zone of the capital. „From a long-term view the decline in the planned construction may be for the hotel market an advantage because it reduces the possibility of market saturation,“ adds to it Jean-François Laporte – Associate Director CBRE Hotels.

Occupancy and average prices decline

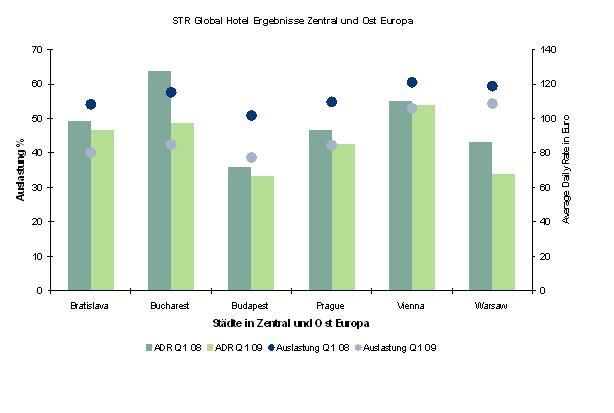

Neither the economy results for hotels in major

cities of the Central nor the Eastern Europe (CEE) are not of the reason for joy

for their owners or operators from the summer of 2008. The data published by STR

Global and TRI Hospitality Consulting on the hotel market in the concerned

region for the 1st quarter of 2009 show a further decline – in terms of both

the occupancy and the average daily rate (ADR) as well.

Neither the economy results for hotels in major

cities of the Central nor the Eastern Europe (CEE) are not of the reason for joy

for their owners or operators from the summer of 2008. The data published by STR

Global and TRI Hospitality Consulting on the hotel market in the concerned

region for the 1st quarter of 2009 show a further decline – in terms of both

the occupancy and the average daily rate (ADR) as well.

Use of Viennese hotels declined in the first quarter of 2009 versus the same period in 2008, approximately by 12.6 percent. This decrease partially relates to the drop in the number of passengers at the international airport in Vienna (the 1st quarter of 2009: –14.8 %!). First, the visitors from Spain, Italy and the United States decreased significantly.

In comparison with other cities in the Central and the Eastern Europe, however, the Vienna hotel market recorded a relatively low loss. Remarkable here is that the revenues from available room (RevPAR) in the international hotel chains are decreasing significantly in comparison with the overall hotel market in Vienna. Based on the Revenue Management Systems and the strength of the individual hotel brands, however, the increase of individual hotel chains turnover is expected in the summer of 2009.

Increasing offer contributes to a vacancy

In Bratislava, Budapest and Prague, in comparison

with the 1st quarter of 2008 (Bratislava: –25.8% Budapest: –24.1% Prague:

–22.9%) the level of hotels utilization in the 1st quarter of 2009 fell by

more than 20 percent! Compared to the same period of last year the number of

passengers at the Bratislava Airport decreased up to 30 percent! Prague

hoteliers also complain, who say about substantial decrease in the number of

tourists from Britain and the USA. In compared major cities of CEE region the

hotel occupancy rate in the 1st quarter of 2009 fell the most in Bucharest, by

26.4 percent. In addition the average daily rate (ADR) decreased in the

metropolitan areas for the period. Its most significant drop recorded in the

monitored period in Warsaw and Bucharest (-21.6% and –23.6%), where the local

currency lost its value significantly compared to the Euro or U.S. dollar.

In Bratislava, Budapest and Prague, in comparison

with the 1st quarter of 2008 (Bratislava: –25.8% Budapest: –24.1% Prague:

–22.9%) the level of hotels utilization in the 1st quarter of 2009 fell by

more than 20 percent! Compared to the same period of last year the number of

passengers at the Bratislava Airport decreased up to 30 percent! Prague

hoteliers also complain, who say about substantial decrease in the number of

tourists from Britain and the USA. In compared major cities of CEE region the

hotel occupancy rate in the 1st quarter of 2009 fell the most in Bucharest, by

26.4 percent. In addition the average daily rate (ADR) decreased in the

metropolitan areas for the period. Its most significant drop recorded in the

monitored period in Warsaw and Bucharest (-21.6% and –23.6%), where the local

currency lost its value significantly compared to the Euro or U.S. dollar.

Adrian Flück, the analyst with CB Richard Ellis Hotels in Prague, stressed: „The number of guests in hotels is constantly decreasing. Business travellers and tourists are also much more sensitive to prices. But the offer of hotels in the cities of the Central and the Eastern Europe continues to grow, so the decline in occupancy and average daily rate (ADR) is not surprise from this view. “

CB Richard Ellis Hotels

CBRE Hotels Company specialized for the Central and

the Eastern European markets; provide expert advices on complex projects in fast

time deadlines and on a professional level. Its dynamic knowledge provides

access to international capital markets, investors and opportunities around the

world. CBRE Hotels services include the selection and meeting with operators,

development and construction of planned hotels and last but not least, always

needed evaluation of existing and planned projects within the frame of

investment consultancy. Its activities include the provision of necessary

services related to the sale and purchase of hotel estates.

CBRE Hotels Company specialized for the Central and

the Eastern European markets; provide expert advices on complex projects in fast

time deadlines and on a professional level. Its dynamic knowledge provides

access to international capital markets, investors and opportunities around the

world. CBRE Hotels services include the selection and meeting with operators,

development and construction of planned hotels and last but not least, always

needed evaluation of existing and planned projects within the frame of

investment consultancy. Its activities include the provision of necessary

services related to the sale and purchase of hotel estates.

Illustration photo – J&T

Graf – CBRE

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook