An area and a layout of unsold apartments is the memento for the future

„The housing market is almost stopped,“ comment real estate brokers with one voice the current alarming – by holidays multiplied – recession of really carried out transactions with the secondary apartments. Said lapidary: if one year ago 10 candidates were queuing to observe 1 apartment, now for the „favour“of 1 candidate on his cognitive marathon seek for 10 apartments at least. And that the seller's market has changed to the buyer’s market is apparently confirmed by his behaviour: You will not cheapen? No need – I have 9 more convenient and better offers!

Developers did not size up a structure of demand

This situation is largely applied to new buildings, too. The earliest development, however, may change it soon, if not reverse. Suspension or revocation of announced residential projects, which will automatically cause the capacity decline on the side of supply, will reveal the current latency of seemingly no existed demand and will trigger its sharp increase again with time. The buyer will hand over the role of dictating boss to a seller involuntarily in this case, what will not be again the balanced state, the parity one, i.e. the healthy state.

Till now, however, specifics to anomalies restrain such scenario realizing, which are for Bratislava residential market typical for several years and to which brings a little more light paradoxically the crisis. For example, to the factual structure and typology of the demand for new buildings, which some developers estimated incorrectly and from their large apartments became idle goods expressively presenting the depth and magnitude of their error.

Buyers refused the inadequateness of the supply

Not far from this finding are the survey results brought by Lexxus Company, monitoring new residential construction from publicly available sources and information, in the report on the residential property market in Bratislava. According to it the low number of projects conforming requirements of the demand causes that the average decrease of the total supply will be only 1–2 percent, while most other projects sell almost nothing. "Today is 858 unsold flats in the 34 completed projects. In the next 12 months should be completed other 50 projects, of which still about 2 700 apartments are unsold, „warns the mentioned report.

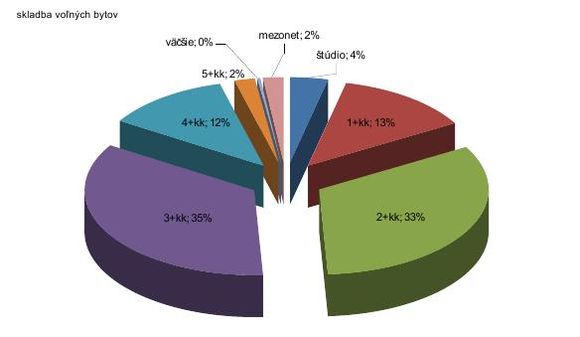

Long-awaited almost constant number of the free – ergo unsold apartments symbolizes the inadequacy of the current supply. Despite the optimal focus on the categories 2kk and 3kk, just these compose their significant part, because they are due to excessive area and unsuitable layouts unattractive, but expensive, and thus hardly marketable (as also illustrated by the pie chart on the composition of free apartments). The following tabular data on the size of available completed apartments are in fact a graphic explanation of this stalemate and so little the lesson for the future that modesty on all sides is never to the detriment.

Rate of sales is slowing down semi-quarterly

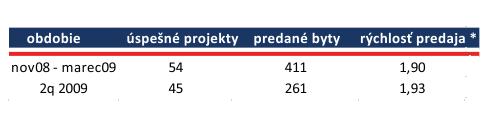

While converting per the number of projects the demand measured by rate of sales is clearly declining. The semi-quarter slowdown (1Q – 2Q 2009) is also expressed by the decrease of the rate from 0.7 of a flat to approximately 0.6 of a flat per a project according to Lexxus Company. Although the number of housing projects, for purchase of which is still an interest is narrowing, their sale in this framework, by contrast, accelerates. This is actually quite logical: the projects which fell in disfavour or remained more or less unnoticed, forward sales of those – which, whether as a result of mass psychosis or uncontested merits – literally are sold like hot cakes. The result is the monthly statistic of sale from 60 to 100 apartments, but in less and less projects.

It is not also needed to neglect the factor of the year-season effect on the demand, which culminated at the end of 1Q (198 sold flats); after a quarter later, however, experienced the significant weakening (63 sold flats). This general decrease is illustrated in the table n°2.

Rate of sales = number of monthly sold apartments per 1 success project

The price cut compared to „the second-hand“ negligible

While the prices of the average 3-roomed apartment on the so-called secondary Bratislava market experienced a drastic break during the past 12 months (brokers prefer the term „making the market more real“) by the order of 1.2 million, the average price of one m2 in new houses fell only negligibly – by about 4 percent. But it has not projects cheapening on its mind, as Lexxus warns, but sells of smaller apartments and increase of the apartments’ ratio with otherwise higher the final, but lower the unit price in the cell ‚free‘. Although the average price of a new apartment m2 is currently around 2080 Euro (62 662 SKK), VAT excluded, semi-quarterly observed development of sales (1Q 2 076 – 2Q 1 840) indicates that the demand directs to the number 1 666 Euro (50 000 SKK), VAT excluded.

At the end of the survey LEXXUS tried to do something what everyone rather avoids now: the prognosis. As the starting point it took the bare statement that in the last 12 months about one third of projects did not sell any apartment or lost more clients than they gained. And so it comes to the conclusion that the guilty party is not the demand, but to it untailored offer. „The slacken demand of the non-existing target group returns developers slowly to reality,“ points out the report and sees the future in such projects, which can address not only by its location and standard, but especially by its area and functional layout. The final price adequate to the product and particularly to the buyer possibilities – like that imagine the final state, within the frame of opportunities optimal, the survey creators, mapping the complicated residential market in Bratislava.

Illustration photo – author Chart and tables – LEXXUS a.s.

Chart – The current composition of free (= unsold) apartments in Bratislava Table n°1 – Areas of available completed apartments Table n°2 – The success of projects and marketability of apartments in the monitored periods

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook