Retail: Developers´ hardship to be continued

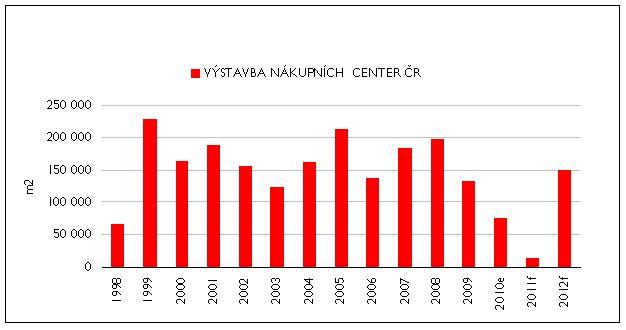

Insistent carol playing and Christmas bell jingles are again attracting thousands of gift-hunting customers to retail centres and parks. For retailers, this year´s Christmas is better than last year, however, “retail“ development has literally wept over its earnings this year. And the outlooks are even worse: there were only new 76,000 sqm in shopping centres and 53,000 sqm in shopping parks in the Czech Republic, although according to qualified estimates, it will be less than a third of this area in the coming year.

CR is no exception this respect, a slowdown in retail construction is apparent everywhere. Across Europe, shopping centres increased only by 6 million sqm this year, which represents a yoy decline of 17 %. And it should continue to worsen in 2011. “The slowdown in construction is a European trend. Approximately 5.2 million sqm of new shopping centre area should be built in Europe next year, this is the lowest number in the last thirty years,“ says Jan Kotrbáček from the consultancy Cushman & Wakefield. According to him, the situation in the Czech Republic will be very similar although with a different background: “We expect the lowest volume of new construction since 1998. This is a new situation after years of fast growth when we were catching up with western Europe.“ And his colleague Alexander Rafajlovič adds: “Next year property developers in the Czech Republic will limit their activities to expansion of current projects, no new shopping centre will be opened for the first time since 1990.“ A small consolation may be the fact that the numbers mentioned include only shopping centres, not shopping parks or retail projects in city centres (a shopping centre according to the definition of International Committee of Shopping Centres (ICSC) is a property with a total leasable area of more than 5,000 sqm with a minimum of ten individual retail units. The overall poor situation will thus be rescued by shopping parks, construction of 15 more is planned but this is only a weak plaster. The crisis in the economy – including the Czech economy – although it is recent but still history, will affect the Czech retail development fully next year. This is of course by virtue of the fact that a shopping centre project usually takes three to four years to complete.

Legend: e – estimate, f – forecast

Source: C&W, Czech Statistical Office, Economist Inteligence Unit estimates

Harfa´s promises

In the current conditions, the recent – traditionally extravagant opening of the Harfa shopping gallery in Prague´s suburb of Vysočany – was an exceptional occasion for the market and almost the only – apart from Chomutovka in Chomutov – well audible tone. (The only other projects worth mentioning are the expansion of Forum in Liberec and perhaps the Van Graf department store at Wenceslas square in Prague.) As already mentioned, nothing like this is expected in the retail market next year. "The spontaneous growth has ended, the market will now grow naturally. There won´t be construction across the board throughout the country,“ states Alexander Rafajlovič. There will be less new construction altogether, there is not much space on the Czech market in terms of expansion. Even on the contrary – according to CB Richard Ellis data, there are 700 sqm of shopping centres per 1,000 inhabitants in Prague. This is indicator is at 250 sqm in the entire Czech Republic which roughly corresponds to EU average where it ranges between 200 and 250 sqm per 1,000 inhabitants. Taking into account buying power of the population and the still difficult and uncertain economic situation (although the Czech Republic was relatively little affected by the crisis), there is very little space for new construction in the coming year. This makes it more imperative for property development and especially shopping centre operators to pay increased attention to quality. “We expect developers to build projects of architectural quality in well visible places in the city centres,“ says Alexander Rafajlovič and Jan Kotrbáček adds: “Owners of shopping centres today focus mainly on making their projects more attractive and on differentiating from their competitors, they are trying to bring in new brands and they put more emphasis on quality centre management.“

Given the high market saturation, new construction will also have – although minimum in the foreseeable future – a bigger effect and impact on the existing projects in the given region or location than before. The first region where a major card shuffling will occur in the coming years, will be probably the Moravian-Silesian region, mainly due to the project Nová Karolina. “I think it is a question of time before developers find courage and start talking about replacing areas which are obsolete – in our conditions rather morally than physically,“ A. Rafajlovič describes the retail development of tomorrow. According to him, future development may be facilitated by a shift in financing: “Banks are already friendlier than in 2009 when nearly all financing stopped. Today it is less complicated to obtain financing, however, it is easier for strong centres or segments which are considered more resistant or more stable, e.g. DIY markets or discount markets.“ His words are confirmed by the recent KPMG survey results in the financial sector – according to it banks´ managements in the Czech Republic prioritize retail development project.

Largest shopping centres in Prague

| Shopping centre | Leasable area in m2 |

|---|---|

| SC Letňany | 125,000 |

| Nový Smíchov | 60,000 |

| Centrum Chodov | 55,000 |

| Metropole Zličín | 52,400 |

| Galerie Harfa | 49,000 |

| Centrum Černý Most | 46,000 |

| Arkády Pankrác | 45,000 |

| Avion Shopping Park Praha | 40,000 |

| Palladium | 39,000 |

| Galerie Butovice | 35,000 |

| Europark Štěrboholy | 33,000 |

Source: CB Richard Ellis

Inside commercial complexes

If the retail project development sector is bleak, the mood is no better in the completed shopping centres. Landlords must increasingly deal with tenants unable to pay rents and on the other hand, they are pushed to decrease rent or provide some incentives by those who prosper even today. Their difficult situation is of course exploited also by new tenants. “Such favourable conditions for business expansion will not be repeated for long. This is why new potential tenants negotiate much longer lease periods than before. Until recently, five-year contracts were common, today there is an increasing number of contracts for ten or twelve years crowned by a five-year option clause. So they are in principle twenty-year contracts,“ said Robert Sninčák from ING Real Estate Investment Management at a recent Stavební fórum discussion meeting. According to him, the crisis is also “cleaning“ the ranks of tenats and landlords – bad projects are more and more faced with vacancy, poor payment discipline of the tenants and high problems of “death“ of lease contracts in case of tenant´s insolvency. Retail building owners are required to pay much more attention to lease contracts. “The value lies in a contract, not the building itself!“ – R. Sinčák pointed out the direction of potential investors´ thoughts. The quality of lease contracts, until recently somewhat neglected, will be today and tomorrow the cornerstone of success – according to the mentioned seminar participants – for shopping centre owners or at least prevention of major problems with “bad“ tenants. According to R. Sninčák, one must “negotiate, negotiate, negotiate!“ with them too, due to the overall market situation.

On the contrary, good news for owners and investors of larger retail units is the arrival of new tenants. For example, new shops of the brands F&F, Swarovski, Claire´s, Burger King emerged in Prague´s Palladium. Brand new tenants have been noticed elsewhere, e.g. brands LegoWear, Prénatal and Cacao Sampaca had their opening in the Harfa shopping centre. Not surprisingly, they are dominated mainly by fashion brands. These have always played the main role in this sector. According to data by Incoma GfK, there are 2,044 fashion shops in roughly three hundred Czech shopping centres, followed by a huge margin by 774 catering establishments, 637 shoe and leather goods shops; followed by jewellery, watch a gift shops (524), electronics and computer shops (480) and grocery shops (442).

“Most varied“ shopping centres

| Shopping centre | Number of retail units |

|---|---|

| Centrum Chodov | 213 |

| NC Letňany | 186 |

| Olympia Brno | 177 |

| Nový Smíchov | 165 |

| Palladium | 153 |

Source: Incoma GfK

The interest of newcomer brands in quality retail space lead to weaking the pressure on rent decrease. Given the important role played by shopping centres in retailers´ expansion plans in the country and taking into account the negligible new construction in 2011, I dare say that fall in rents in the best shopping centres is not an issue owners should deal with,“ claims Alexander Rafajlovič. Monthly rent per square metre in a Prague shopping centre where prices are logically highest, starts at approximately EUR 30, ie. roughly CZK 738, according to November figures by CB Richard Ellis. This is how much traders pay for example in the shopping gallery Nové Butovice, one of the least visited shopping centres. On the contrary, the highest rent is in the Palladium shopping centre in the centre of the capital. One square metre there costs on average EUR 85 per month (about CZK 2,093).

In the future, however, it will not be only about commercial offer, tenant mix (and the amount). We can count on the fact that the concept of shopping as a pastime will become increasingly important. A role in the fight for customer will also play the offer of sports and cultural events, or outlets. Harfa shopping centre vehemently admits to the shopping – entertainment concept with their slogan “Harfa gallery – this is where you live“. It will probably be the first to offer its visitors a roof terrace of 9,500 sqm serving as a leisure zone, where Dinopark will be soon.

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook