Predicting recovery of the market: alternately cloudy, cloudiness temporarily...

The estimates, when appear serious signs of the approaching end of the economic crisis are noticeably similar to the current weather forecasts. One really has a lot to choose from, but nobody knows it certainly guarantee that the undertone ray of sun means an irreversible course to a lasting light or only momentary clarification in the legendary „hurricane eye“, followed by another, usually even more devastating act of cataclysm. So the conclusions from the statistics contained in the reports of consulting companies are offering every moment different updating its outlook forecasts.

CBRE: Warehousing and logistics facilities gape due to emptiness

Occurrence of certain exceptions, which we wrote in Friday’s article about, yet not negates validity of the rule that the projects of logistics and warehousing facilities are constantly exposed to fluctuations in financial markets and bank financing. While the total area under construction remained unchanged in the 3rd quarter of 2009 over the previous period in Slovakia, in the semi-year comparison to be talking already about 50 percent decline. So many rigorous but concise numbers of the latest report of industrial consultation-estate firm CB Richard Ellis (CBRE).

Yet harder looks the volume of works implemented in 3rd quarter: 13 thousand m2 through three transactions, which represented 78% of semi-quarter and 80% of semi-year decline. Most of these volumes are, as traditionally, the transactions in the Bratislava region. As for the CBRE report notes on the other hand, a smaller volume of transactions coupled with the relatively low supply led to a stable rate of non-occupancy 11.03%.

Prices of rents to historic minimums!

Expected change will affect developers of modern

storage and logistics areas so that instead of speculative construction will

begin to prefer tailor-made solutions what someone already do (the mentioned

PointPark Propereties for Möbelix). Fighting for a client according to CBRE

likely in a short term will force developers to sign leases for a shorter period

or lower rents. Effective net rent in modern storage halls in Slovakia remains

in the range of 3 to 4.5 € / m2/month depending on location and competition

around. As a fundamental reversal in the market is not too soon to expect, when

approving loans the banks will remain vigilant with regard to the percentage of

projects pre-renting.

Expected change will affect developers of modern

storage and logistics areas so that instead of speculative construction will

begin to prefer tailor-made solutions what someone already do (the mentioned

PointPark Propereties for Möbelix). Fighting for a client according to CBRE

likely in a short term will force developers to sign leases for a shorter period

or lower rents. Effective net rent in modern storage halls in Slovakia remains

in the range of 3 to 4.5 € / m2/month depending on location and competition

around. As a fundamental reversal in the market is not too soon to expect, when

approving loans the banks will remain vigilant with regard to the percentage of

projects pre-renting.

"Many areas recently gape due to emptiness. On the one hand it caused exaggerated expectations of developers and speculative projects, on the other hand, the ongoing crisis and the consequent reduction in the interest of end users of such spaces. Developers were forced to attract bids to lure on new candidates. Prices of rents got to their historic minimum and the fact that almost nothing new is developed and non-occupancy is slowly declining, it is probably the best time for prospective tenants to accelerate their decision to lease these premises, "said Peter Jánoši, the head of industrial properties of CBRE.

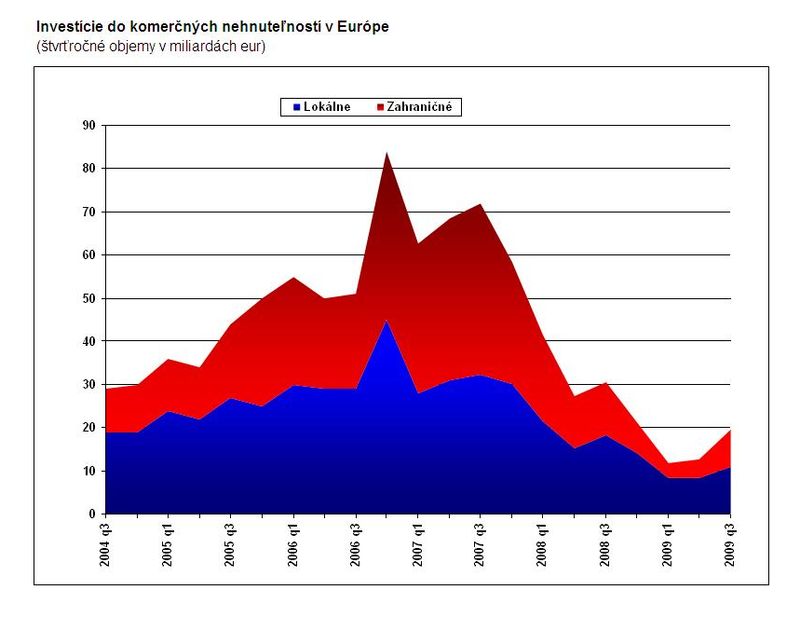

C&W: Returned trust is accompanying an increase in the volume of investments

The European real estate market is finally beginning to burgeon green shoots of recovery – the volume of investment in real estate jumped by 53% in the 3rd quarter, revenues stabilized and the labour market had stimulating development that is close to stability at least, says the new report of the global surveys leader – Cushman & Wakefield (C & W) – on the development of investments in the European market for commercial real estate. Her optimistic spirit, however, encourages sceptical question whether the desire in this case does not anticipate reality

„Although the market is still facing several problems, but after two quarters of growth and with a much better mood, it is clear that we have overcame a major milestone,“ refutes any doubts, James Chapman, the head of capital markets department of C&W in SR and CR. What is the supporting argument for him? „Revenues will stabilize at a level that is for buyers with long-term objectives and interests of equity, clearly attractive, and still more people believe that although the market of tenants has not reached the bottom yet, it is time to act.“

Stabilization of revenues will also bring improvement in the capital growth development Chapman, however, immediately points to a small hitch: the lack of supply, while the banks provide loans, but many sellers do not hurry with sales – hoping that prices will „get better“. And so he concludes that despite the increasing volume of investment in 2nd half of 2009 the expectations for 2010 remain continue conservative.

Availability of financial menas will improve prospectively

Regarding the outlook, Chapman expects that the

focus of traditional foreign investors in income-generating assets will

continue, particularly in Western markets. Probably, however, they will

increasingly bother the lack of products on offer. Investors will be forced to

revise their expectations regarding the returnability and approach to risk. This

may be an advantage for the Slovak market in 2nd half of 2010 in conjunction

with their return.

Regarding the outlook, Chapman expects that the

focus of traditional foreign investors in income-generating assets will

continue, particularly in Western markets. Probably, however, they will

increasingly bother the lack of products on offer. Investors will be forced to

revise their expectations regarding the returnability and approach to risk. This

may be an advantage for the Slovak market in 2nd half of 2010 in conjunction

with their return.

Another plus in the Chapman’s vision ought to be continually improving availability of loans for new acquisitions, which in 2010 reportedly contribute to even extending the market recovery. Already now, increases their willingness to lend, either separately or in pools of larger projects (already referred support of VÚB Bratislava for PointPark at Lozorno). Although credit conditions remain relatively restrictive, the competition in lending will involve more and more banks. Uncertain is the question of refinancing existing loans, when banks start to claim a refund of their money because some owners fail to secure it, believes James Chapman.

First class facilities will be dealt first

The most attractive segment of the market remain office space, where the volume of transactions increased by 87% to 10.6 billion € in the 3rd quarter. It is expected that by the end of 2009 will represent about 90% of the total volume in the Central Europe. Significantly also increased the area of industrial property, while retail trade was in terms of financial market characterized by particular lack of quality products and demandingness of major projects such as shopping centers, by C&W. German institutions and open-end funds remain in Slovakia an under-represented foreign group – because of fear of economic instability and a relatively small market.

Eastern markets are leaders in the trend of reducing the rent for lucrative premises where they has fallen by 29 percent at average. „When once the dust starts settle after the economic collapse, some candidates will decide that it is the right time to use their market power and provide better facilities, which we are now witnessing,“ says David Hutchings, the head of the European research group of C&W. Since the offer of the first class facilities is usually less they will be dealt first according to him. In other words it means, the best financial conditions for the best real estate may not be actual long time.

Graphs – CBRE, C&W

1 – Share of developers in the Slovak market for storage properties

(2009/Q3)

2 – Development in the Slovak industrial properties market (2007/Q4

– 2009/Q3)

3 – Investments in commercial real estate in Europe (quarter volumes in

billions €)

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook